Mezzanine Loans – UK Europe United States Australia

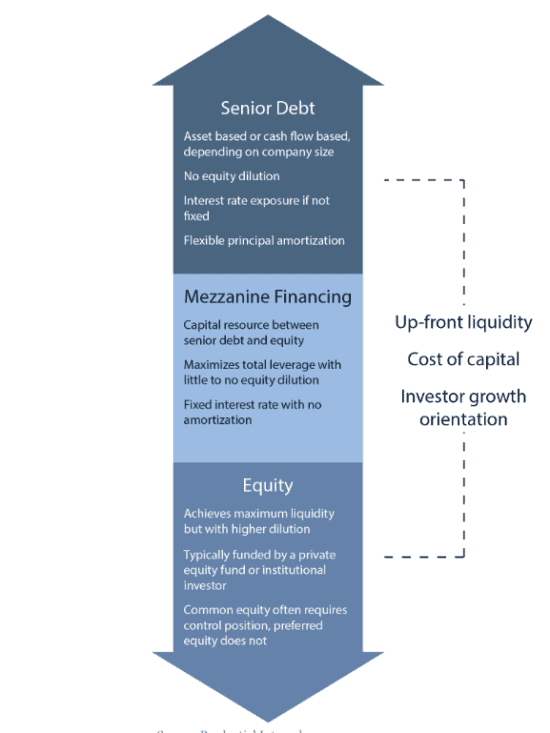

Mezzanine finance is a capital resource that sits between (less risky) senior debt and (higher risk) equity that has both debt and equity features. Companies use mezzanine lending to achieve goals that require capital beyond what senior lenders will extend.

Mezzanine finance is a capital resource that sits between (less risky) senior debt and (higher risk) equity that has both debt and equity features. Companies use mezzanine lending to achieve goals that require capital beyond what senior lenders will extend.

When companies have maximised their senior debt borrowing capacity or seek to preserve future senior debt capacity and need additional capital to pursue growth opportunities (acquisitions, large capital programs, etc.), or for shareholder activity (distributions, shareholder buyout, etc.) they are typically left with two options: raise outside equity or utilise mezzanine financing. Mezzanine financing can be viewed as either expensive (higher coupon) debt or cheap (less dilutive) equity, as mezzanine carries a higher interest rate than the senior debt that companies would obtain through their banks (reflecting greater risk than senior debt), but is substantially less expensive than equity in terms of overall cost of capital. More specifically, mezzanine financing is less dilutive than raising additional equity to satisfy a capital need, and ultimately allows existing owners to maintain control. Mezzanine is patient capital that enables companies to pursue opportunities from a long-term strategic approach, which may not have seemed feasible otherwise.

What is Corporate Mezzanine Financing?

Corporate mezzanine finance is named for its place in the capital structure, mezzanine financing is a form of junior capital that sits between senior debt financing and equity, and is a means by which companies can access capital beyond what they’re otherwise able to achieve on a senior basis. Mezzanine financing is also the last stop along the capital structure where owners can raise substantial amounts of liquidity without selling a large stake in their company.

Mezzanine typically comes in the form of “subordinated debt” or “preferred equity” with a fixed-rate coupon or dividend, and may have some participation rights in the common equity of a business, but is materially less dilutive than common equity.

Although mezzanine financing is more expensive to borrow on a coupon basis than senior debt, it is also more patient, typically carrying a longer term until its final maturity (up to 7-8 years), and is interest-only with no amortisation prior to maturity. This element of “patience” affords a business time to process the growth event or shareholder activity as well as build senior capacity (via increased retained cash flow) to refinance the mezzanine capital over time.

For many businesses, mezzanine is not viewed as permanent capital, but instead solution-oriented capital that serves a specific purpose, and can later be replaced with lower cost capital, i.e. senior debt.

Mezzanine financing is usually unsecured and subordinated to a company’s senior debt (both structurally in terms of its right of repayment, and time subordinated with a longer dated maturity and no scheduled principal amortisation prior to maturity, which leads most senior lenders to consider mezzanine financing as “equity-like,” patient capital sitting behind their facilities. In the event a company is facing liquidity constraints, the senior lender can pause (or “block”) current interest payments on mezzanine debt. These features typically provide a company’s banks or senior lenders with comfort in their senior position, and, as a result, mezzanine financing is often preferred by first lien senior lenders relative to second lien loans or other debt alternatives.

It is common for a private equity firm to provide capital in exchange for majority or complete ownership of a company in situations where mezzanine can be used instead, such as an acquisition or ownership transition. Rather than giving up control of the business, companies can turn to a mezzanine-supported recapitalisation, or “minority recapitalisation,” as an attractive alternative.

Mezzanine financing is ultimately a way for companies to grow faster than they could otherwise on a senior basis alone and also execute an ownership or management transition in a way that allows existing stakeholders to increase their ownership interest.

Uses for Mezzanine Financing

In many situations where senior debt or equity might ordinarily be used, companies can instead turn to mezzanine financing to fulfill their capital needs. It is a patient source of financing that enables businesses to accomplish their goals for growth, whether it is building a larger production facility or accomplishing an acquisition that can’t be completed with all senior financing.

Mezzanine financing provides incremental leverage to facilitate a wide variety of transactions, including the following:

- Recapitalisations

- Leveraged buyouts

- Management buyouts

- Growth capital

- Acquisitions

- Shareholder buyouts

- Refinancings

- Balance sheet restructuring or optimisation

Mezzanine Pricing & Payment Structure

Mezzanine financing is more expensive than senior debt and cheaper than equity, but is a relative hybrid of the two, so it is priced as a blend of both senior debt and equity. Mezzanine is most commonly subordinated debt, or subordinate to senior debt, with maturity occurring a year after the senior debt. It is typically structured to include a mixture of contractual interest – cash and payment-in-kind (PIK) and nominal equity (warrants). It often has a bullet maturity with no amortisation during the life of the loan.

Companies will often utilize senior debt capacity that is built up over time to refinance the mezzanine loan prior to maturity, reducing the cost of their debt capital in the process. However, the longer maturity and lack of any required amortisation of the mezzanine loan also provides important capital structure “patience” for the business to process the financing event (such as integrating an acquisition).

Mezzanine Financing Pros and Cons

For a company considering introducing mezzanine financing to their balance sheet, it’s wise to weigh the pros and cons to best determine whether mezzanine is the right fit for their business.

Pros:

- A mezzanine-led recapitalisation often results in the existing owner retaining majority control of the company, controlling the board, management, etc.

- Mezzanine financing provides more flexibility (looser financial covenants, reduced amortisation, fewer restrictions) than traditional bank loans and allows companies to achieve goals that require capital beyond senior debt availability

- It is less costly and less dilutive than a direct equity issuance (institutional equity typically has a return expectation of 20%+)

- With mezzanine, companies have an alternative capital resource to senior debt and equity

- Mezzanine is “patient” capital that supports long-term growth with interest only for up to seven or eight years and no amortisation

- There are fewer control type provisions than typical minority private equity

Cons:

- Mezzanine financing is more costly than senior debt

- Mezzanine financing may involve some equity dilution, which is typically small, and may be in the form of attached warrants or some other structure

- Terms for a mezzanine financing include financial covenants and creditor rights

- There is often a prepayment penalty for a period following issuance

Selecting a Mezzanine Financing Provider

There are important considerations for a company when determining whether to take on mezzanine financing. When choosing a lender or investor, some key characteristics to look for are:

- Because mezzanine financing supports long-term growth, it is vital for the mezzanine financing provider to have the capacity to grow as a financial partner and have the knowledge and experience to help a company navigate through challenging times

- They are relationship-oriented rather than transaction-oriented. It’s important that the mezzanine financing provider show interest in supporting the long-term strategies of the companies they finance as well as work to understand the needs of the businesses and how they function

- They are fast-acting, responsive and have access to key decision-makers within their organisation

- The mezzanine financing provider has a demonstrated track record of delivering mezzanine capital throughout market cycles and the calendar year

- They follow through on their commitments

- The provider has in-depth experience investing in a variety of industries and can tap into that experience when approaching your business needs

- Ultimately, it is most important to find a mezzanine financing provider who will be a strong partner that supports the goals of your company.Whether expensive debt or cheap equity, mezzanine financing is a viable option for companies that need additional capital but don’t want to sell the business or lose control. Like other offerings, mezzanine financing is patient capital that nurtures business growth for the long term.

Click here to visit next page Global Aircraft Financing and Leasing